IndiGrid is the first Infrastructure Investment Trust (“InvIT”) established to own power transmission assets in India. IndiGrid owns 16 independent revenue-generating elements, including 13 transmission lines of 3,360 ckms and 3 substations of 7,000 MVA capacity across 9 states in India. We believe that access to reliable power is a fundamental right as it is the lifeline of human productivity and ingenuity.

Article:

Infrastructure Investment Trusts, or InvITs, as they are better known, offer an attractive investment opportunity for investors to earn stable income from longterm infrastructure assets. On the other hand, InvITs provide infrastructure developers the much-needed platform to monetize their operating assets in order to free up debt capacity to undertaking more development projects. InvITs can be a game changer for the Indian power sector which is facing severe stress. InvITs not only offer developers a robust platform to divest their operating assets, but it also offers investors the ability to invest in stable operating infrastructure assets. This flow of capital could work wonders for the power sector. Since Securities and Exchange Board of India (“SEBI”) notified the InvIT Regulations, there have been three InvIT issuances till date which has raised ~ INR 10,000 Cr. These InvITs are backed by strong sponsors like Sterlite, L&T and IRB.

IndiGrid is the first Infrastructure Investment Trust (“InvIT”) established to own power transmission assets in India. IndiGrid owns 16 independent revenue-generating elements, including 13 transmission lines of 3,360 ckms and 3 substations of 7,000 MVA capacity across 9 states in India. We believe that access to reliable power is a fundamental right as it is the lifeline of human productivity and ingenuity. Our business of owning power transmission projects is directly enabled by connecting critical load centers to generating centers.

InvITs were launched with the objective of developing an alternate means of financing for infrastructure projects. The entire infrastructure spend of the country has been either financed by banks or public spending, which results not only in asset liability mismatches, but also in restricting the acceleration of new infrastructure development. This is the area where InvITs can truly be the game changer for the infrastructure sector in India. InvITS have the potential to transform the way infrastructure is financed in India. Given the recent events in infrastructure financing, it’s imperative to consider InvITs as a credible option to invest and cultivate and expedite the development of infrastructure in India.

InvITs are a true win-win-win forinvestors-developers-India as they provide investors with a good long-term stable investment opportunity, opportunities for developers to deleverage and release locked-in capital to grow, and India to have incremental investment in underdevelopment infrastructure projects.

Yield platforms: a global success

The operating framework behind InvITs and REITs builds on the experience of similar instruments (i.e. YieldCos, Master Limited Partnerships (“MLP”), Business Trusts, etc.) that have been around for many decades in developed financial markets like the USA, the UK, Australia, Singapore and Hong Kong. We have seen around 70 listings of similar platforms in the neighbouring countries like Singapore, Hong Kong and Malaysia, where these platforms have been prevalent for the last 10-15 years.

Globally, there are over 400 listings of similar instruments accounting for over US$ 1 trillion of investments. These instruments have assisted countries to meet their capital needs for the infrastructure and real estate sectors. Long-term infrastructure assets like roads, power generation, telecom towers, power transmission, warehouses, ports, gas pipelines etc. are owned by such platforms which offer investors stable income and growth for long-term. They are considered as high dividend-paying investments suitable for investors looking for long-term, stable cash flow with moderate capital appreciation.

Attractive long-term investments

There are three salient aspects of InvITs that make them an attractive platform to invest: Low Risk, Predictable Distribution and Robust Corporate Governance.

Low Risk

InvITs primarily invest in operating and revenue-generating infrastructure projects. SEBI requires InvITs to invest at least 80% of their AUM in completed and revenue generating projects, and not more than 10% of their AUM in under-construction projects. As most of its investments are in operating and revenue-generating projects, InvITs are not exposed to some of the key risks inherent in the infrastructure sector like financial closure, construction delays, regulatory approvals, and cost overruns, etc. Low risk in InvITs is also evident from the fact that all the three InvITs – IndiGrid, IRB InvIT and Indinfravit, are rated AAA by CRISIL, India ratings and ICRA.

Predictable distribution

SEBI requires InvITs to distribute a minimum of 90% of their cash earnings to investors at least semi-annually. As most concessions for infrastructure projects are long-term, it offers investors a frequent and predictable distribution over a long period of time.

“INDIGRID OWNS 16 INDEPENDENT REVENUE GENERATING ELEMENTS, INCLUDING 13 TRANSMISSION LINES OF 3,360 CKMS AND 3 SUBSTATIONS OF 7,000 MVA CAPACITY ACROSS 9 STATES IN INDIA”

Corporate governance: independence, unit holder rights & disclosure requirements

InvITs are managed by an Independent Trustee and an Investment Manager, appointed by it, on behalf of the unit holders. The Board of the Investment Manager comprises of at least 50% independent directors to ensure independence from its Sponsors.

The Investment Manager is required to publish valuation of all assets by an Independent Valuer on a bi-annual basis and include it in the half-yearly report. Most of the critical decisions like acquisition of new projects, leveraging beyond 25% of asset value, change of independent valuers, further unit issuances etc., require the approval of a majority unit holder. In the case of related party transactions like acquiring new projects from the Sponsor, the governance framework requires positive votes from a majority of non-Sponsor unit holders. Sponsors do not have voting rights in such matters.

Owing to the above characteristics, InvITs are perfectly suited for the institutional investors like insurance companies, pension funds, foreign portfolio investors, mutual funds and corporate treasuries. InvITs are also suitable for non-institutional investors who prefer high dividends. For non-institutional investors like HNI or retail, InvITs also provide a regulated platform to invest in income yielding infrastructure assets, which is otherwise not available due to the scale and sophistication required for such direct investments. Further, InvITs enjoy zero capital gains tax if the units are held for over three years and sold through the stock exchange.

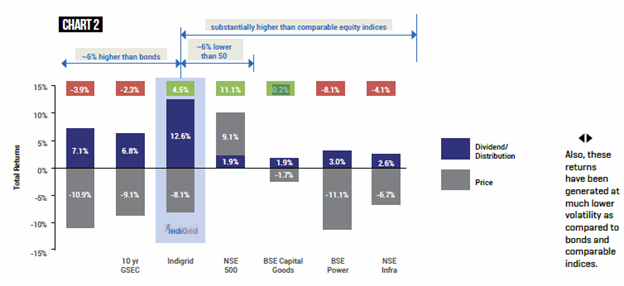

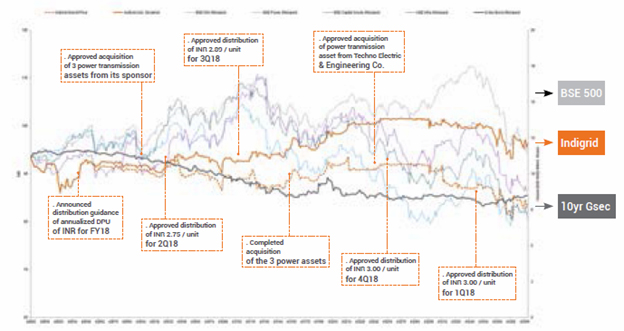

Performance since listing: predictable distribution and low volatility

Performance of InvITs is largely dependent on the underlying assets and stability of its cash flows. For example, IndiGrid which owns power transmission assets, has annuity like cash flows for 35 years with no price or volume risk.

Chart 2 show cases the low volatility of IndiGrid compared to comparable indices since listing. In addition to being less volatile, the total return* delivered by IndiGrid is substantially higher than the government securities as well as comparable equity indices even in an increasing interest rate scenario.

*Total return = Distribution/ Dividend paid by security + change in price during the period. There have been 6 quarterly distributions made by IRB InvIT and IndiGrid since listing.

Road Ahead

India has already invested over INR 70 lakh crore in building different infrastructure assets across roads, ports, power transmission, airports, railways etc., over the last few decades. InvITs provide a robust alternate source of financing for the much-needed infrastructure development in India, which has a crying need of US$ 1.5 trillion over the next decade. InvITs can help reduce the dependence on bank financing while also providing the financial community with a credible investment opportunity.

Global investors prefer to invest in operating infrastructure projects which earn stable yield. A successful market of InvIT will draw billions of dollars in the country from foreign institutional investors and provide the much-needed fillip for the development of the infrastructure sector of India.

Whilst the Government of India has played a monumental role in making InvITs and REITs a reality in India, a few regulatory changes would go a long way in cementing the attractiveness of InvITs. Despite the initial success, InvITs are far from achieving their true potential. Several companies like ILFS/ITNL, Reliance Infra, GMR and ACME Solar could not pursue the InvIT route to raise capital.

“SEBI REQUIRES INVITS TO INVEST AT LEAST 80% OF THEIR AUM IN COMPLETED AND REVENUE GENERATING PROJECTS, AND NOT MORE THAN 10% OF THEIR AUM IN UNDER CONSTRUCTION PROJECTS”

From the experience of listed InvITs till now, we believe that the 49% cap on leverage is inhibiting investors to invest in InvIT. Investors prefer investing in similar assets under AIF or equity platform which provides higher returns due to no such leverage restriction. Even international instruments comparable with InvITs – Business trust, YieldCo, MLP in Singapore, the USA, the UK, and Australia, do not have any such leverage restrictions. Such restrictions only exist for REIT platforms globally. If the regulators consider higher than 49% leverage with a base rating like “AA+” by two or more rating agencies, the attractiveness of this new financial instrument will increase without increasing their risk profile. This will provide an impetus to infrastructure developers to favourably consider setting up new InvITs.

The government along with the regulators must do their utmost to ensure the success of InvITs, given the long-term potential of these instruments as alternative sources of infrastructure funding. InvITs could not only alleviate the NPA problem that the banking sector is grappling with, but also enable the government to monetize its existing infrastructure assets. This robust capital market instrument has credible potential to spur the much-needed infrastructure development of India.

Article source: Infraline plus – November, 2018 issue.

Please wait...

Please wait...