Sterlite Power – Latest News, Press Release, Photos & More

Sterlite Power News

Our news repository will show case the latest information on regulatory and policy changes, technology in transmission, information on our projects and our impact through our work.

New Delhi, 10th October 2023: Sterlite Power, a leading power transmission developer and solutions provider in India and Brazil, announced the appointment of Ruhie Pande as the Group Chief Human ...

– New orders secured in domestic market and international regions like Americas, European Union,Africa, and Middle East. – Decarbonization and greening the grid are the primary growth drivers. New Delhi, ...

New Delhi, 22 nd September 2023: Sterlite Power, a leading power transmission developer and solutions provider in India and Brazil, announced the acquisition of Beawar Transmission Limited, a Special Purpose Vehicle ...

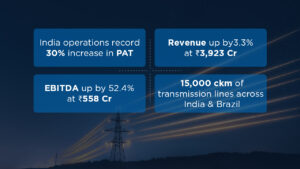

New Delhi, 12th September 2023: Sterlite Power, a leading power transmission developer and solutions provider in India and Brazil, announced its results for the year ending 31 st March 2023. The ...

Please wait...

Please wait...